Best SCRM Tools & Software for Highly Regulated Industries (2026 Comparison)

Summary

A comprehensive overview of the best Supply Chain Risk Management (SCRM) tools and software for highly regulated industries available in 2026, with an assessment of standout features and appropriate industry applications. This guide is aimed specifically at highly regulated industries and highlights the importance of loss quantification capabilities as well as standard risk scores. It includes an at-a-glance table followed by a more detailed assessment of eight leading providers.

Introduction

In the past, supply chain risk management (SCRM) was a world of reactive firefighting. Modern tools have changed all of that, with the best providing better data visibility and analytics, faster alerts and scenario-planning capabilities that allow risks to be far better managed. Highly regulated sectors will need advanced features more than most. Compliance, product integrity, patient safety and extensive documentation requirements mean that disruptions carry greater consequences and must be avoided or mitigated wherever possible.

One capability that's increasingly critical – for all sectors – is loss exposure quantification. While many platforms offer risk identification and alerting, fewer provide the sophisticated modelling needed to estimate location-based exposures with insurance-grade accuracy. This is crucial for CFOs and boards who need to understand exposure in terms of profit, not just in terms of risk scores.

We encourage you to assess your specific requirements, request demonstrations from shortlisted vendors and involve stakeholders from risk management, compliance, procurement and IT in the evaluation process.

Comparing the Leading SCRM Platforms

The at-a-glance table below evaluates eight leading SCRM platforms across key capabilities. We've graded loss exposure quantification capabilities from basic (✔️) to intermediate (✔️✔️) to advanced. Following the at-a-glance table, we look at each tool in detail.

Full Disclosure: SCAIR® is one of the platforms featured in this comparison, and we naturally have an interest in helping organisations discover our functionality. However, we've made every effort to present an objective assessment of the leading SCRM tools available today, according to specific requirements.

| Tool / Platform | Loss Exposure Quantification (‘How Much Will This Cost’) | Node Vulnerability Analysis (Where Are We Most at Risk’) | Climate / Environmental Risk | Key Differentiators | Best For |

| Coupa LLamasoft | ✔️✔️ What-if scenario modelling | ✔️ End-to-end visibility | ✔️ Advanced environmental disruption analytics | Supply chain network optimisation, forecasting | Enterprises needing integrated planning |

| Riskmethods (Sphera) | ✔️✔️ Impact Analyzer module | ✔️ Risk Radar for supplier profiling | ✔️ ESG risk management | AI-driven alerts, customisable dashboards, compliance monitoring | Mid-to-large enterprises with ESG focus |

| SCAIR® | ✔️✔️✔️ Deterministic loss modelling | ✔️ Node-level exposure mapping | ✔️ Scenario-based modelling (climate events) | Supply chain mapping, impact analysis, concrete financial impact estimates | Pharma, aerospace, high-regulation sectors |

| Everstream Analytics | ✔️✔️ Predictive analytics for disruption impact | ✔️ Global supply chain visibility | ✔️ Natural disaster & geopolitical risk modelling | AI-powered insights, real-time data feeds | Dynamic, global supply chains |

| SAP IBP | ✔️✔️ Scenario planning & simulations | ✔️ Inventory and demand forecasting | ❌ Limited (requires integration) | ERP integration, advanced analytics | Large enterprises with SAP ecosystem |

| Jaggaer | ✔️ Automated risk response plans | ✔️ Supplier/product-level risk scoring | ❌ No direct climate modelling | Spend management, supplier benchmarking | Procurement-heavy organisations |

| Resilinc | ✔️✔️ Event impact prediction | ✔️ Multi-tier mapping | ✔️ Natural disaster modelling | EventWatch, RiskShield, capability assessments | Supplier performance & disruption recovery |

Legend: ✔️✔️✔️ = Advanced | ✔️✔️ = Intermediate | ✔️ = Basic | ❌ = Not available or limited

Coupa LLamasoft ‘Best for existing Coupa platform users’

Coupa's platform integrates supply chain optimisation with risk management, offering powerful hypothetical modelling capabilities. The system uses advanced analytics to assess how environmental disruptions could impact operations, then suggests alternative sourcing or routing strategies.

Standout Features: The combination of risk management with design and forecasting tools means organisations can simultaneously optimise for efficiency and resilience.

Integration with Coupa's broader procurement platform creates a unified view.

Best For: Large enterprises seeking integrated planning and risk mitigation within a single ecosystem, particularly those already using Coupa for procurement.

Riskmethods (Sphera) ‘Best for companies with ESG reporting requirements’

Riskmethods brings AI-driven insights to supply chain risk management through its Risk Radar and Impact Analyser modules. The platform provides supplier profiling with customisable dashboards that can be tailored to specific compliance requirements.

Standout Features: Strong ESG risk management tools make this platform particularly relevant for companies facing increasing regulatory pressure around sustainability and social responsibility. The customisable compliance monitoring can be configured for industry-specific regulations.

Best For: Mid-to-large enterprises with significant ESG reporting requirements and organisations in industries where supplier ethical practices carry regulatory or reputational risk.

SCAIR® ‘Best for pharma and highly regulated industries’

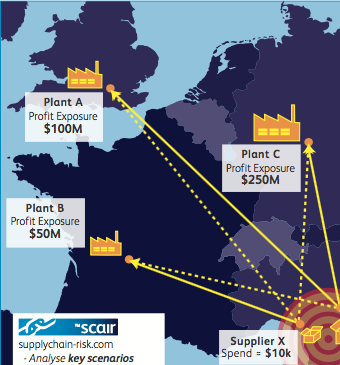

SCAIR® was purpose-built for highly regulated industries, with pharmaceutical companies comprising a significant portion of its client base. Five of the top 20 global life sciences companies by revenue either use SCAIR® as part of their annual review process or have used SCAIR® for criticality studies. The platform's defining characteristic is its advanced loss modelling – this is the most sophisticated impact quantification capability in the market. It also leverages the power of Munich Re’s Location Risk Intelligence, to provide location-specific natural hazard and climate change scores.

Standout Features: Node/building-level exposure mapping combined with scenario-based modelling (including climate events) allows risk managers to identify vulnerabilities at granular supply chain points. The platform translates disruption scenarios into concrete financial impact estimates, providing the quantitative data that boards and insurers require.

One of the most notable elements of SCAIR® is the availability of complementary consultancy to help organisations get the most from the platform. Integrating the tool with help from the SCAIR® team can promote a new, organisation-wide methodology and mindset towards greater resilience.

Best For: Biopharmaceutical, medical devices, nutraceuticals and other highly regulated sectors where precise loss quantification, regulatory compliance and board-level risk reporting are paramount.

Everstream Analytics: ‘Best for businesses with fast-changing supply chains’

Everstream leverages AI-powered insights and real-time data feeds to provide predictive analytics for disruption impact. The platform offers global supply chain visibility with particular strength in natural disaster and geopolitical risk modelling.

Standout Features: Machine-learning algorithms continuously analyse patterns to predict potential disruptions before they occur. The real-time data feeds pull from diverse sources, including news, weather and geopolitical intelligence.

Best For: Organisations with dynamic, global supply chains that change frequently and need continuous monitoring across multiple risk dimensions simultaneously.

SAP Integrated Business Planning (IBP) ‘Best for large enterprises with established SAP infrastructure’

For enterprises deeply embedded in the SAP ecosystem, IBP offers scenario planning and simulation capabilities that integrate directly with existing SAP systems. Inventory and demand forecasting capabilities are particularly robust.

Standout Features: Seamless integration with SAP ERP systems means data flows automatically without manual export/import processes. Advanced analytics leverage the full breadth of enterprise data already captured in SAP systems.

Best For: Large enterprises with established SAP infrastructure who want risk management integrated into their broader planning processes.

Note: Climate modelling capabilities are limited and typically require third-party integrations.

Jaggaer ‘Best for cost-conscious procurement’

Jaggaer approaches SCRM through a procurement lens, offering automated risk response plans and supplier/product-level risk scoring. The platform's strengths lie in spend management and supplier benchmarking.

Standout Features: For procurement-heavy organisations, Jaggaer's integration of risk management with spend analysis provides insights into how risk mitigation strategies affect procurement costs. Note: climate and environmental risk modelling capabilities are not a direct feature of this platform.

Best For: Organisations where procurement teams drive supply chain decisions and where spending optimisation is a critical risk management priority.

Resilinc ‘Best for organisations focused on supplier performance management’

Resilinc has built strong capabilities in incident alerting and multi-tier supplier mapping. The platform's EventWatch feature provides real-time monitoring of global disruptions, while RiskShield offers scenario-based capability assessments.

Standout Features: Natural disaster modelling combined with multi-tier mapping helps organisations understand cascading impacts through their supply network. Supplier performance tracking aids in disruption recovery planning.

Best For: Organisations focused on supplier performance management and rapid disruption recovery, particularly those in industries where second- and third-tier supplier visibility is critical.

Key Considerations for Highly Regulated Industries

When evaluating SCRM platforms for regulated sectors, several factors deserve special attention:

Loss Exposure Quantification Capabilities: Can the platform translate supply chain scenarios into concrete financial impact? This capability is essential for board reporting, insurance discussions and capital allocation decisions. Platforms vary significantly in their sophistication here – from basic ranking scores to full risk quantification.

Compliance and Audit Trail: Does the platform support the traceability requirements specific to your industry? Pharmaceutical companies need a different level of audit tracking than aerospace manufacturers.

Integration Capabilities: How well does the solution integrate with your existing ERP, PLM and quality management systems? Data silos undermine risk visibility.

Trend Analysis: Can the system provide year-on-year change and trend analysis, with the accompanying justification for the change?

Scenario Modelling Sophistication: Can you model complex, multi-variable scenarios including climate events, geopolitical changes and regulatory shifts simultaneously?

Visit our platform overview at https://supplychain-risk.com/ to learn more about our specialised approach to pharmaceutical and highly regulated industry supply chain risk management.