Hormuz and the Hidden Risks to Pharma Supply Chains

The conflict in Iran has illustrated that it’s not just the industry’s reliance on Indian APIs that creates vulnerabilities for pharma supply chains.

The US and Iran may be closer to a deal as a fragile ceasefire just about stands, but uncertainty over supplies isn’t going away any time soon.

President Trump has announced he is stopping US operations to escort stranded vessels out of the Strait of Hormuz in order to firm up a deal with Iran, but the US blockade of Iranian ports continues.

More than 20 ships have been attacked near the Strait of Hormuz since the start of the conflict. On the same day as the US President announced the ceasefire extension, Iran said it had seized two cargo ships in the strait, which it refuses to open due to the US naval blockade.

While it stays closed, an oil crisis is rapidly escalating into a more profound chokehold on global supply chains.

Pharmaceutical Supplies Face Shortages

Even in March, UK commentators were warning of imminent issues for the supplies of generic medicines.

As Moody’s analytics director of supply chain management told the Guardian, “It's the perfect storm. We have the conflict in the Gulf that caused the Strait of Hormuz to shut down and India is known as the pharmacy of the world.”

The Iran conflict has also hit at a time when supply chains were already under strain. As far back as December, Aspirin shortages were already being felt in the UK, for example. By January, a National Pharmacy Association (NPA) survey was finding that 86% of pharmacies could not fulfil aspirin requests.

Drug shipments headed to the Middle East have been affected first, but Western markets are also vulnerable, particularly where there is a dependence on one geographic region for an API. And even while supplies continue, costs are escalating.

“While we are not currently seeing exceptional shortages, manufacturers are facing sharp increases in transportation costs, particularly for air freight,” Mark Samuels, Chief Executive Officer at Medicines UK, said back in March.

The switch from higher prices to all-out shortages could be rapid, however. The head of NHS England told LBC he was “really worried”, given the country relies on imports for three quarters of its drug supplies. Already, some drugs, such as those used to treat Parkinson’s, are experiencing supply issues.

Generic Dependencies

As Moody’s analysis indicates, much of the issue is modern dependence on India for generic medicines and active pharmaceutical ingredients (APIs). That, of course, is not news, and has long been a concern before most of us could have pointed to the Strait of Hormuz on a map.

The dependence on India (and China) is well recognised – if not easy to address.

It’s not just Western dependence on India and China at question, either, but dependencies between the two. India (the world’s biggest generics exporter) depends on the Strait for much of the crude oil imports its pharma businesses rely on, but also for chemical raw materials produced in China. These are often consolidated in Dubai and the UAE and then shipped to India.

As this piece details, even in mid-March, amoxicillin trihydrate (a penicillin API) prices were up 45% in a week; paracetamol active pharmaceutical ingredient prices increased 26%; diclofenac sodium (used in anti-inflammatory NSAID) rose by as much 30% percent; and ciprofloxacin (fluoroquinolone antibiotic) prices were up by as much as 30% since December.

In the UK, meanwhile, shortages of carbon dioxide, which has myriad uses, including in medical procedures, prompted the government to invest £100m to reopen a manufacturing site for the gas that was mothballed last September.

Solvents and Hidden Supply Chain Vulnerabilities

The crisis has highlighted the complex nature of modern pharmaceutical supply chains and multiple points of vulnerability. The dependencies on key APIs have long been obvious; pharma companies will know their exposures off the top of their heads. But aside from APIs, what about acetonitrile, the solvent that “runs through nearly every HPLC [high-performance liquid chromatography] and LC-MS [liquid chromatography-mass spectrometry] in every lab and QC [quality control] suite in every pharmaceutical company on earth”.

As the writer puts it, “[F]or researchers, pharmaceutical chemists and CDMO production teams, the real concern is different and more immediate: the reagents, solvents, and process chemicals used daily in synthesis, purification and analysis – almost all of which connect, within a handful of synthetic steps, to Gulf feedstocks.”

The piece details the escalating impact as disruption continues:

- Wave one in which methanol, ammonia, formaldehyde, acetic acid, formic acid, chlorine, HCl, caustic soda and sulphuric acid all see immediate price increases.

- Wave two, where solvents and reagents such as DMF, acetonitrile, NMP, hexane and IPA become more expensive or become restricted.

- Wave three in which Fmoc amino acids, coupling reagents, specialty monomers, fluorinated building blocks and other advanced intermediates see the same.

As the writer makes clear, supplies don’t need to dry up for there to be a problem, and the crisis isn’t just for generics: “For academic groups on fixed grants, CROs pricing fixed-fee contracts, and CDMOs managing campaign economics, this kind of systemic cost inflation is harder to manage than any single shortage, because there is no single substitution that resolves it.”

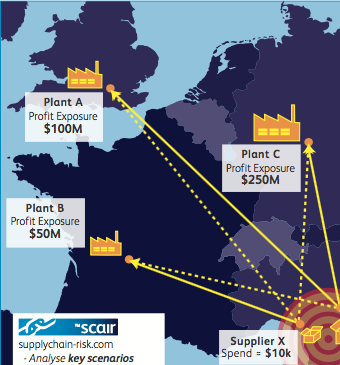

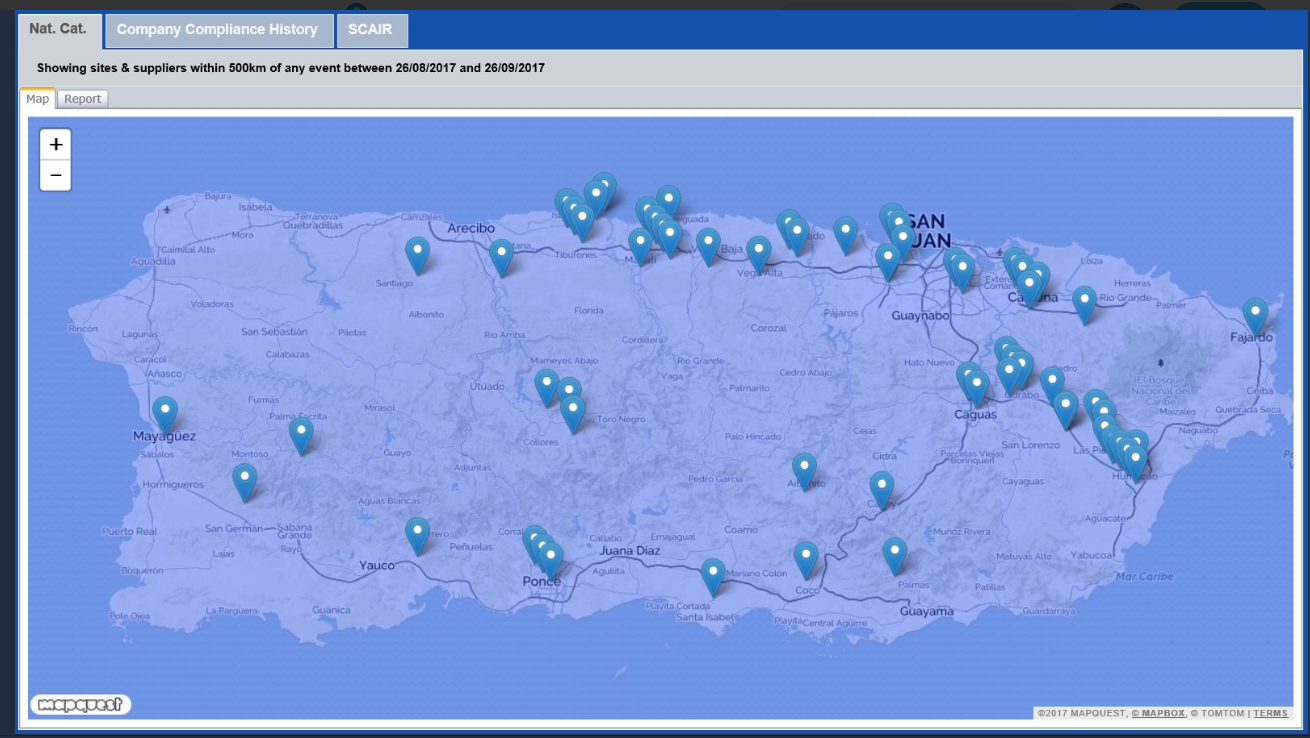

See Dependencies with Supply Chain Risk Management Software

These are, though, new wrinkles to old and widely recognised problems. And they are not going away, whatever happens with the Iranian ceasefire and flows through the Strait of Hormuz.

As we’ve seen countless times, reliance on global sources is essential for constraining costs of generic drugs right across pharmaceutical supply chains. Critical dependencies are difficult to untangle, and not all vulnerabilities can always be managed. At the very least, pharma businesses cannot escape rising prices.

But visibility of the supply chain, dependencies, vulnerabilities, pinch points and, crucially, value at risk is essential. Without it, businesses are unable to distinguish between avoidable and unavoidable vulnerabilities or make informed decisions about where to invest in mitigation or insurance.

The issues around solvents and reagents, in addition to APIs, highlight the difficulties of achieving this without using the technological tools available. Solutions such as SCAIR® are designed to enable organisations to have the end-to-end visibility of supply chains that they need. They can then identify common dependencies on APIs or manufacturing sources to plan alternatives, and the key – and potentially not obvious – vulnerabilities in their supply chains. They can, crucially, also calculate the value at risk to make informed decisions about mitigation and insurance.

When dealing with complex supply chains and a volatile world, such tools give the best chance of navigating your business through dangerous waters.